Web cookies (also called HTTP cookies, browser cookies, or simply cookies) are small pieces of data that websites store on your device (computer, phone, etc.) through your web browser. They are used to remember information about you and your interactions with the site.

Purpose of Cookies:

Session Management:

Keeping you logged in

Remembering items in a shopping cart

Saving language or theme preferences

Personalization:

Tailoring content or ads based on your previous activity

Tracking & Analytics:

Monitoring browsing behavior for analytics or marketing purposes

Types of Cookies:

Session Cookies:

Temporary; deleted when you close your browser

Used for things like keeping you logged in during a single session

Persistent Cookies:

Stored on your device until they expire or are manually deleted

Used for remembering login credentials, settings, etc.

First-Party Cookies:

Set by the website you're visiting directly

Third-Party Cookies:

Set by other domains (usually advertisers) embedded in the website

Commonly used for tracking across multiple sites

Authentication cookies are a special type of web cookie used to identify and verify a user after they log in to a website or web application.

What They Do:

Once you log in to a site, the server creates an authentication cookie and sends it to your browser. This cookie:

Proves to the website that you're logged in

Prevents you from having to log in again on every page you visit

Can persist across sessions if you select "Remember me"

What's Inside an Authentication Cookie?

Typically, it contains:

A unique session ID (not your actual password)

Optional metadata (e.g., expiration time, security flags)

Analytics cookies are cookies used to collect data about how visitors interact with a website. Their primary purpose is to help website owners understand and improve user experience by analyzing things like:

How users navigate the site

Which pages are most/least visited

How long users stay on each page

What device, browser, or location the user is from

What They Track:

Some examples of data analytics cookies may collect:

Page views and time spent on pages

Click paths (how users move from page to page)

Bounce rate (users who leave without interacting)

User demographics (location, language, device)

Referring websites (how users arrived at the site)

Here’s how you can disable cookies in common browsers:

1. Google Chrome

Open Chrome and click the three vertical dots in the top-right corner.

Go to Settings > Privacy and security > Cookies and other site data.

Choose your preferred option:

Block all cookies (not recommended, can break most websites).

Block third-party cookies (can block ads and tracking cookies).

2. Mozilla Firefox

Open Firefox and click the three horizontal lines in the top-right corner.

Go to Settings > Privacy & Security.

Under the Enhanced Tracking Protection section, choose Strict to block most cookies or Custom to manually choose which cookies to block.

3. Safari

Open Safari and click Safari in the top-left corner of the screen.

Go to Preferences > Privacy.

Check Block all cookies to stop all cookies, or select options to block third-party cookies.

4. Microsoft Edge

Open Edge and click the three horizontal dots in the top-right corner.

Go to Settings > Privacy, search, and services > Cookies and site permissions.

Select your cookie settings from there, including blocking all cookies or blocking third-party cookies.

5. On Mobile (iOS/Android)

For Safari on iOS: Go to Settings > Safari > Privacy & Security > Block All Cookies.

For Chrome on Android: Open the app, tap the three dots, go to Settings > Privacy and security > Cookies.

Be Aware:

Disabling cookies can make your online experience more difficult. Some websites may not load properly, or you may be logged out frequently. Also, certain features may not work as expected.

Professor Langlois’s book Advanced Introduction to the Economics of Organization has been published in the Elgar Advanced Introduction series:

This incisive book presents a succinct overview of the economics of organization. Combining traditional approaches with more challenging, cutting-edge perspectives, Richard N. Langlois critically examines the ways in which tasks and transactions in the economy are organized.

Drawing on a diverse array of historical and real-world examples, chapters outline key principles of the field including division of labor, transaction costs, moral hazard, and asset specificity. This Advanced Introduction investigates ‘organization’ more broadly, delving into underexplored areas such as capabilities and routines, evolutionary selection, dynamic transaction costs, and modular systems.

Photo: Bradford, Phillip G. 2023. “Chains that Bind Us”. Amazon Publishing, book cover. Used with permission of the author.

Students in Professor Smirnova’s “Money and Banking” course were exposed to a discussion about the block-chain technology from a viewpoint of the computer science as Dr. Phillip Bradford, Computer Science Professor at Stamford, delivered an engaging lecture “Chains that Bind Us” on February 27, 2025.

Professor Bradford connected the history of blockchains to the history of payment systems and functioning of Central Banks in an economy. He helped students understand the appeal of anonymous but verified ledgers of transactions, and linked such economic concepts as money supply, inflation, and economic growth to the development of various blockchain technology based “coins” and their fluctuating value in the market.

Professor Bradford demonstrated his Python codes and showed the “Raspberry Pis”, which he used in his experiment of mining bitcoins.

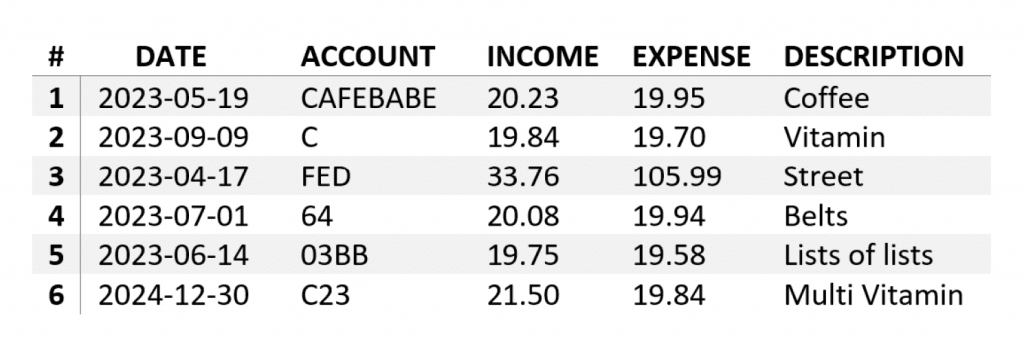

Dr. Bradford intrigued students with a basic ledger such as shown in Figure 1.

Figure 1. Basic Ledger (Bradford, 2023, p. 21)

This ledger is itself coded. For example, the first account “CAFEBABE” is a keyword in Java program files. See for example: Java class file – Wikipedia sometimes called a magic number to start Java machine files. Do you see any code for #3 account “FED”?

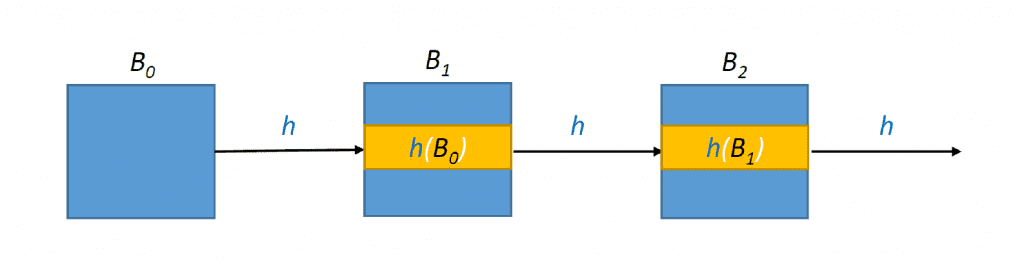

Such ledgers are in each block of a block chain such as shown in Figure 2.

Figure 2. Blockchain (Bradford, 2023, p. 116)

The curriculum of the “Money and Banking” course focuses on the Federal Reserve System, the central bank of the United States, its policy tools, goals, strategy and tactics, and on the banking system as a participant in the country’s financial system. An exposition of new and emerging technologies that provide alternatives to central banking is an exciting addition to the course. Students are using Dr. Bradford’s book “Chains that Bind Us” (Bradford, 2023) as a supplemental reading material to the required textbook (Mishkin, 2022).

Such multi-disciplinary collaborations among faculty strengthen our learning community at the Stamford campus. Co-authoring papers and presentations, monthly multi-disciplinary colloquia, and visits to classes support diverse interests of our students that will be joining the workforce with career-transferable knowledge and skills.

Bibliography:

Bradford, Phillip G. 2023. Chains that Bind Us. Amazon Publishing.

Mishkin, Frederic S. 2022. Economics of Money and Banking Economics of Money, Banking, and Financial Markets, 13th edition, Pearson.

In this paper, Professor Zhao and his coauthors examine an often-overlooked driver of economic inequality: health disparities. They show that health inequality is not just a reflection of broader economic disparities but a key driver of them.

Abstract:

Using a dynamic panel approach, we provide empirical evidence that negative health shocks significantly reduce earnings. The effect is primarily driven by the participation margin and is concentrated among the less educated and those in poor health. Next, we develop a life cycle model of labor supply featuring risky and heterogeneous frailty profiles that affect individuals’ productivity, likelihood of access to social insurance, disutility from work, mortality, and medical expenses. Individuals can either work or not work and apply for social security disability insurance (SSDI/SSI). Eliminating health inequality in our model reduces the variance of log lifetime (accumulated) earnings by 28 percent at age 55. About 60 percent of this effect is due to the impact of poor health on the probability of obtaining SSDI/SSI benefits. Despite this, we show that eliminating the SSDI/SSI program reduces ex ante welfare.

UConn Storrs 2024 Team: from left to right: back row: Professor Derek Johnson (faculty adviser), Spencer Thompson, Viren Chainani, Lilla Korniss, Claire Dobbins, Katrina Melnik, Professor Owen Svalestad (faculty adviser). Front row: Nameeda Elmi, William Infante, Evelyn Zhou and Rai Kumar

The Economics Department students participate in the College Fed Challenge national competition every year. The Storrs team competes in the Boston district of the Federal Reserve System, and the Stamford team competes in New York. In 2024, the Storrs team was a National Finalist, which is an exceptional achievement. In February 2025, both teams travelled to the Board of Governors of the Federal Reserve System in Washington, DC, for an Open House for all participants.

UConn Stamford 2024 Team: from left to right: back row: Matthew Dalzell, Thomas Surette, Angelina Solodka, Professor Smirnova (faculty adviser), Paul Juszczyk, Liz Maia, Madina Mamedli, Brenda Leon, Mallory Albrecht, front row: Cole Sembrot and Micthell Velasco.

In addition to summarizing results from the 2024 competition, the agenda of the Open House focused on showcasing various segments of the Fed’s functions and sharing career opportunities available at the Board for graduates with bachelor’s degrees. Participants heard from Brian Bonis, Assistant Secretary of the FOMC, Matt Eichner, Director of the Division of Reserve Bank Operations and Payment Systems, and a panel of former Fed Challenge participants, who are now employed as Research Assistants (RAs) at the Board.

The students of both teams were excited to participate in the Open House and are appreciative of the Economics Department as well as other entities that provided funding for this trip. The sponsors are the Business School, CLAS Dean’s Office, UConn Center for Career Readiness and Life Skills, and Stamford campus administration. Thank you!

During the trip to the Open House at the Federal Reserve Board, UConn-Stamford 2024 Team of the College Fed Challenge competition had an opportunity to meet with UConn alum, Misbah Seyal. Mr. Seyal is a real estate professional with a substantive career including various positions at Moody’s, Wells Fargo, Bank of America, and other financial services firms.

Natalia Smirnova, faculty, (left) and Misbah Seyal, UConn alum (BA’97, MBA’04), at dinner with students on February 6, 2025, in Washington, DC.

During the meeting with students, Misbah talked about career opportunities after graduation from UConn. He emphasized the importance of developing skills that could be transferred to the workplace and of being adaptable to labor market conditions as they change.

Students were interested in learning about the real estate sector as well as about the financial sector. They were curious about navigating the competitive market environment and about balancing career expectations and family. Misbah shared his wisdom and encouraged students to pursue their passions and dreams.

The students, as well as Dr. Smirnova, faculty adviser to the College Fed Challenge team, are grateful to Mr. Seyal for his time with us. We are also appreciative of Ms. Siobhan Lidington, Director of Development, School of Business, University of Connecticut Foundation, for her efforts to make this meeting possible.

Professor Thomas Miceli has published Harm and Responsibility: The Economic Factors Controlling the Extent of Civil and Criminal Liability

From the publisher:

Risk is an ever-present feature of life in a complex world, and it is important for societies to manage it in a just and efficient manner. One way to reduce risk is to assign responsibility for the associated harm. In this book, economist Thomas J. Miceli examines harm and responsibility from an economic perspective.

The book focuses on how responsibility affects people’s incentives to refrain from causing unnecessary harm to achieve what economists call optimal deterrence. Secondarily, it is concerned with the quest for justice. Defining this is part of the journey. Does it mean compensating victims for unavoidable losses? Does it involve punishing wrongdoers in proportion to the harm they have caused? Is there a clear answer? The book addresses these questions and more, explaining how, in some cases, these objectives will align with deterrence and in others they will not. The book discusses the ways that the law, tempered by religious and social norms, strikes a balance between these goals.

The principal areas of law that assign legal responsibility are tort law (for accidental harms) and criminal law (for intentional harms). There exist vibrant economic theories of both, and this volume draws on this literature. One theme that emerges is the role of causation in determining responsibility. Attributing responsibility for a given harm to the party that caused it seems both morally just (because it embodies personal responsibility), and economically desirable (because it achieves deterrence in the most direct manner). And yet the law departs from this prescription in any number of ways, both by limiting the responsibility of some who caused harm and by expanding responsibility to some who did not. The book offers readers coherent economic explanations for these departures from a purely causal basis for legal responsibility.

Author Thomas J. Miceli clarifies causation as reciprocal in nature and therefore not a uniquely defined concept. This means that when an action by A causes harm to B, the question is not how to restrain A but rather: whether A has the legal right to take the action in question or whether B has the right to prevent it. There will be a harm either way; the relevant question is which party should bear it. This insight ultimately leads to the fundamental problem of defining harm. In most conflicts this can be straightforward—as when A punches B—but in others it is more challenging. For example, when does free speech become hate speech? Where is the line drawn?

The book concludes by drawing out the implications of this fundamental ambiguity over the meaning of harm, what that means for the law, and what economic theory has to say about it.

Public Economics students, (from left to right), Brendan Tuite, Abigail McDonough, Isaias Juarez, and Yukun Zhang, present their findings in class on November 19, 2024, Stamford campus

During the Fall 2024, the students in the ECON 3431- “Public Economics” course at the Stamford campus worked with the industry professional to research, analyze, and propose policy solutions to the imminent State of Connecticut problem of Solid Waste Management.

The applied nature of the course allowed students to experience every aspect of public policy development from problem identification, ideation, research of the literature, data gathering, analysis, and policy recommendation formulation.

In addition to Professor Smirnova, who is the instructor of this course, the students worked under the mentorship of Mr. Brian Bartram (CLAS’ 94), who has been the manager of the Salisbury/Sharon (CT) Transfer Station in Connecticut since 2007. At that time Salisbury & Sharon were seeking design ideas to be used in the construction of a new transfer station. Since then, Brian has been active in the Northeast Resource Recovery Association, CT Department of Energy & Environmental Protection’s Solid Waste Advisory Committee, and CT Product Stewardship Council. In 2012 he was appointed by Gov. Malloy to be a member of the Modernizing Recycling Working Group. Brian completed the UConn Master Composter Program in 2015.

Students were assigned to groups to imitate the economic think-tank work environment. Each group selected their topic through the process of ideation based on Brian’s presentation about the acute waste management problem in Connecticut. The following research questions were formulated and answered during the semester:

Cost Benefit Analysis of Installing a Methane Capture System at the Manchester, Connecticut Landfill.

Government Policies Promoting Recycling and Landfill Use Reduction.

Where Did Your Old TV Go?

What is the Most Cost-Effective Waste Conversion Technology for Connecticut Municipalities?

How does Connecticut Dispose of Waste Tires?

Public Economics students, (from left to right), Sam Jenkins, Jordi Silva, Hannah Geary, and Kyle Nelson, present their findings in class on November 19, 2024, Stamford campus

At the completion of the course, student teams presented their findings to the class with Mr. Bartram visiting the class virtually, asking questions, and commenting on issues. Brian reflected that he “really enjoyed how different student teams were looking at the issue from different angles. Solid waste is a national, regional, state, and local issue. All different views and situations need to be considered and assessed.”

Through this exercise, students learned to collaborate with and present and defend their findings to the industry expert. Collaborative experiences such as this, between UConn students and the State of Connecticut professionals, are invaluable in preparing our students for careers in industries and the public sector. By integrating the workplace analytical approaches into the curriculum of applied courses, we are teaching students career competencies that are demanded of them upon graduation.

ECE Economics workshop participants in Storrs on October 23, 2024

The Early College Experience – Economics program is the largest at UConn. In the Economics program, we have 34 partner high schools with 66 certified economics instructors. Last academic year, 1,102 students were enrolled in 68 economics courses, with a total enrollment of 1,607 students. Our program is making a meaningful impact on Connecticut students introducing them to economic concepts and way of thinking as well as preparing them for college attendance.

Every year, Dr. Smirnova, who is ECE Economics coordinator, conducts the professional development workshop for participating teachers. The workshop is aimed at providing comparability of instruction and at sharing pedagogical innovations.

This year, 23 teachers from partner schools attended the workshop on October 23. The room was buzzing with commotion as guest speakers engaged the audience with hands-on activities.

Our guest speakers were Ariel Slonim, Curriculum Designer at Marginal Revolution University (MRU) and Mary Clare Peate, Senior Economic Education Specialist at Federal Reserve Bank of St. Louis.

The micro- and macroeconomics concepts were showcased in interactive ways, that would encourage high school students to engage in the classroom. Here are the topics:

Learning about Economic Decision Making with Pretzels

Cowbells and M&Ms: Creative Classroom Exercises for Teaching Externalities and Public Goods

The Inflation Rate is Falling, but Prices are Not!

Fact vs. Fiction: Interactive Tools to Teach the Truth About Fiscal Policy

This year, the teachers also heard from their peer, Ms. Lynn Taillon from Cheshire High School. Ms. Taillon shared her “Valentine’s Day” and “Model Decorations for Christmas” activities. Such sharing stimulated the discussion of other ideas and stories of attending teachers.

Participants went away with a lot of pedagogical materials that could be used immediately in their classrooms. All materials are stored on HuskyCT in the ECE Economics organization section.

Last Thursday, October 17, 2024, the Department of Economics held its regular semester GA Training Workshop, aimed at preparing new Graduate Assistants for their teaching responsibilities. Three faculty members—Professors Talia Bar, Professor Kai Zhao, and Professor Tianxu Chen—shared valuable advice drawn from their teaching experience.

Professor Bar emphasized the importance of adapting to students’ varying levels of mathematical proficiency, using active learning strategies to keep students engaged, and proactively addressing potential classroom challenges.

Professor Zhao reflected on his early teaching experiences, offering advice on understanding student backgrounds, using relatable examples, and ensuring clear communication to avoid confusion.

Professor Chen concluded the session by focusing on classroom management, encouraging a positive learning environment, and balancing teaching duties with academic responsibilities. Her practical tips provided GAs with useful strategies for success.

This workshop remains a cornerstone of the department’s efforts to support GAs, offering them essential tools and insights to excel in both teaching and their academic progress each semester.

Congratulations to the UConn Storrs Fed Challenge team!

Over the past few days, the undergraduate students on the Fed Challenge team competed in the Boston Federal Reserve (Boston Regional) Fed Challenge competition, and they excelled – first advancing to the Boston Regional Finals, and then advancing to the National Finals.

As a result, in November the team members will be presenting their economic forecasts and monetary policy recommendations to the Federal Reserve in Washington, DC. This is an exceptional achievement.

A brief recap of the Boston event… On Friday, October 18th, the team competed with 23 other universities and colleges in the New England Boston Federal Reserve district. For the first round, the 24 teams (universities and colleges) were divided into six groups of four, with the winner of each group moving on to the Boston Regional Finals.

The UConn team won in its group, and earned its spot in the Regional Finals, joining the other five other Regional Finalists (Yale, Harvard, Wellesley, Babson and Dartmouth) to compete in a final round on Sunday. The final round would decide which three of the six Regional Finalists would move on to the National Finals.

UConn competed against the schools in the Regional Finals, presenting analyses of current macroeconomic conditions and monetary policy recommendations and fielding questions from Boston Federal Reserve economists. The UConn team was outstanding, and by the end of the day had made it to the National Finals along with two other teams.

The three New England Universities to move on are Yale, Harvard and UConn.

Congratulations to our student team members for all of their hard work and accomplishments!

The students are:

Viren Chainani (presenter) Spencer Thompson (presenter) Claire Dobbins (presenter) Rai Kumar (presenter) Katrina Melnik (presenter) Nameeda Elmi William Infante Lilla Korniss Evelyn Zhou John Mclean

The faculty advisors are Derek Johnson and Owen Svalestad.

Professor Langlois’s book Advanced Introduction to the Economics of Organization has been published in the Elgar Advanced Introduction series:

Professor Langlois’s book Advanced Introduction to the Economics of Organization has been published in the Elgar Advanced Introduction series: